Building a Central Payment Platform for Retailers

In today’s consumer-driven retail environment, payment technologies are being influenced by both consumers and retailers. Payment platforms have evolved beyond being a simple mean of transmitting funds to becoming added value systems. Retailers are facing global payment challenges and need to build a central payment platform, mainly due to payment models proliferation and consumer behaviour changes. Financials, Data & Security and Innovation aspects are leading this change of payment platform strategy.

“Financials”: retailers are concerned by the cost of “payment”. This includes the costs of the transaction itself (charged by the acquirers) but also the costs of deploying, maintaining and certifying a payment solution over one country or multiple countries and for one or multiple POS vendors. Obviously, being agnostic from both POS vendors and acquirers will tend to facilitate those costs optimisations.

“Data & Security”: retailers need to secure their data (that will tend to grow to big data management, with a central payment platform) and be compliant with PCI-DSS standard.

“Innovation” is a key driver as well, retailers need to support today and tomorrow payment innovation: omni-channel, wallet, biometric… They need to be able to follow up what will be the next payment instrument or payment channel used by their customers.

When retailers made their decision to implement such platform, they do need to look for few fundamental software capabilities to overcome those challenges:

- Omni channel, few examples to illustrate what a true omni channel platform is: platform needs to be able to initiate a transaction on one channel and complete it on another one, or to make a purchase on one channel and reverse it on another one.

- Smart & Dynamic routing of authorisations and transactions to the right acquirer. The right acquirer being the one that offers best pricing for a given transaction. It has to be dynamic and configurable so that retailers can define their own business rules

- Real-time protocol conversion to support the multiple configurations retailers are facing when deploying their platform in their own environment: acceptance platforms, acquirers, countries,….

- High availability: this platform is becoming critical and as such can never stop running

- PCI-DSS certification

A the same time when they build their central payment platform, retailers have now access to new business opportunities that were not easily accessible when their payment platforms were fragmented or just not omni channel… They can now focus on increasing Customer insights: customer data are now consolidated into one place therefore facilitating the purchasing behaviour analysis, the comparison of customer segment #1 versus customer segment #2,… They can launch value added-services (Couponing, Tokenisation, Loyalty, Dynamic Currency Conversion,…) in a much easier way thanks to this unique integration point to address all channels. And some of them could even become their own acquirer by connecting to the schemes directly instead of going through the acquirers.

Finally, there is a growing expectation for new frictionless customer experience such as invisible payment (e.g. AmazonGo), Card Digitalization (e.g. El Corte Inglés card digitalized), ... on top of some others like Card on File that are there for quite some time now to improve customer experience for payment on internet. This is resulting into an increasing number of payment means day after day, driving pressure on merchants regarding how they store payment credentials.

As a matter of fact, Tokenization is becoming a must. Besides increasing greatly customer experience by supporting new forms of payments, new channels… Tokenization allows a couple of significant cost reductions: lower PCI DSS costs (isolate systems using payment data, decreasing exposure to sensitive payment information to other systems) and diminish Payment Costs (risk of fraud is reduced, treat all transactions as Card Present transactions, get a lower interchange).

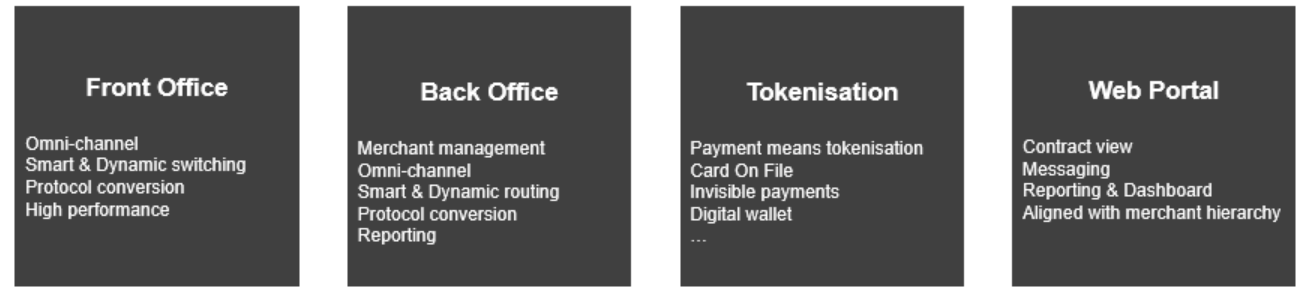

To address all those challenges and opportunities, HPS provides to retailers a flexible and modular platform that relies on 4 building blocks. It is an all-in-one, pre-acquiring and/or Acquiring, Nexo-Ready solution. HPS building blocks include: